Is the independence of central banks in peril?

Is the degree of independence of central banks declining? This rather academic-sounding question is indeed a significant one, at least from a capital market perspective. In the extreme case of a total loss of independence, a portfolio should be exposed as little as possible to the respective monetary system (money market, government bonds, currency). Instead, investors should give preference to asset classes such as gold, Bitcoin, equities, corporate bonds, and government bonds with a high degree of credibility in terms of price stability. Please note: investing in securities involves both opportunities and risks.

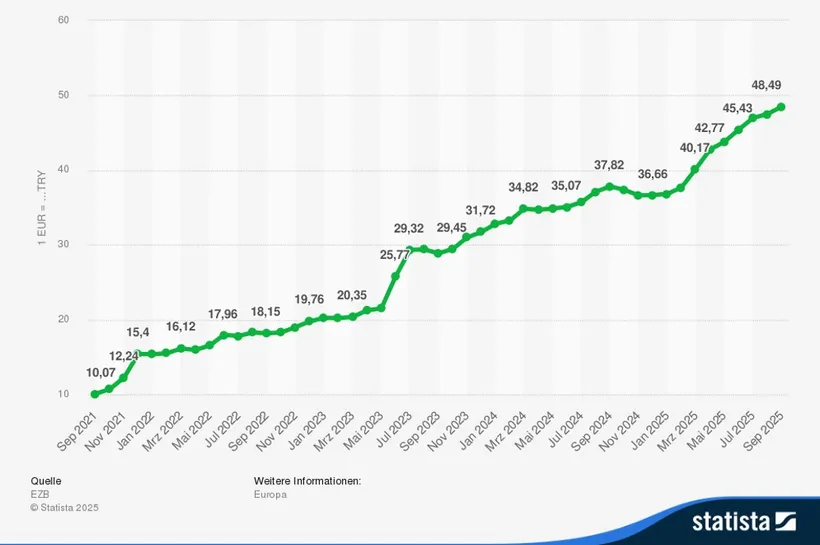

Turkey as a case study: political influence and inflation dynamics

The prices of Turkish government bonds denominated in the local currency, the Turkish lira, have increased by 57% since the beginning of 2021 (source: ICE BofA). At first glance, this seems positive. However, high price increases in the economy have caused purchasing power to fall by 85% and put pressure on the currency (which has depreciated by about 81% against the euro). Bond yields have averaged 23% compared with average inflation of 49%. The inflation-adjusted (real) yield was therefore abundantly negative. In euro terms, the value of Turkish bonds did not rise, but instead fell by just under 71%. In contrast to bonds, Turkish equities (MSCI Turkey) rose significantly (by an annual average of 56%). The inflation-adjusted return on equities was therefore clearly positive (annual average: about 7%). This means that for investors in Turkey, equities provided good protection against inflation. Equity investors from the Eurozone also recorded gains (56% per year in local currency vs. 42% per year of currency depreciation).

What was the main reason for the high inflation in Turkey? Probably politics. President Recep Tayyip Erdoğan has long held the view that high interest rates cause inflation. As a result of this stance, key-lending rates were cut even though inflation was already on the rise.

Monthly development of the EUR/TRY exchange rate from September 2021 to September 2025 (in TRY)

Sources: ECB, Statista, data as of September 2025

Historical perspective: from the gold standard to inflation management

The idea that central banks should be independent is relatively recent. The first central banks, such as the Swedish Riksbank (founded in 1668), the Bank of England (1694), and the Banque de France (1800), were often established as private companies that were granted a monopoly on issuing banknotes by the state. Their main function was to finance government spending, especially in times of war. An independent monetary policy was not envisaged. In the 19th century, the gold standard dominated.

Bretton Woods

After WWII, the Bretton Woods system was introduced, which provided for fixed exchange rates and gave central banks only limited monetary policy autonomy. The system was based on fixed exchange rates, with the US dollar pegged to gold at USD 35 per ounce. In 1971, President Nixon announced the end of the US dollar's convertibility into gold. In 1973, most countries abandoned fixed exchange rates.

Floating exchange rates

This was followed by a transition to floating exchange rates: exchange rates were determined by supply and demand on the foreign exchange market. Central banks would occasionally intervene to stabilise the currency. However, the stagflation of the 1970s (high inflation in combination with stagnant growth) illustrated very well that the monetary policy should not be politically motivated in a system of floating exchange rates. Otherwise, there was a risk of high inflation and currency deprecation. As a result, the monetary policy was increasingly used as an instrument to combat inflation. Central banks such as the German Bundesbank and later the Fed and the Reserve Bank of New Zealand were given more autonomy. From the 1990s onwards, many central banks adopted inflation targets as their monetary policy model. In 1990, the Reserve Bank of New Zealand was the first to have a legally binding inflation target. With the Reserve Bank Act 1989, which came into effect on 1 February 1990, the RBNZ became the first central bank in the world to enshrine an inflation target as its primary monetary policy objective in law. The bank was granted operational independence: it could take monetary policy decisions without direct political influence.

Counterpressure

The post-Bretton Woods era was characterised by increasing market orientation rather than state control, globalisation of the financial markets, and independent monetary policy. However, two developments, one slow and one fast, have been creating a certain amount of counterpressure. Firstly, high and rising government debt and, secondly, the unorthodox policies of the new US administration.

High interest payments

According to the OECD, interest payments on government debt across the OECD area will increase to 2.7% of nominal gross domestic product (GDP) this year. This figure was last reached in 2000. The difference to that time, however, was that the government budget excluding interest payments (the primary balance) amounted to 1.8% of GDP at that time. The estimate for this year is minus 1.6%. This results in an estimated overall state budget deficit of 4.3% for this year (2.7% interest payments plus 1.6% primary deficit). As most countries have so far shown little effort to reduce their budget deficits (see, for example, the USA and France) and interest payments are likely to continue to rise, budget deficits are likely to remain high for the foreseeable future.

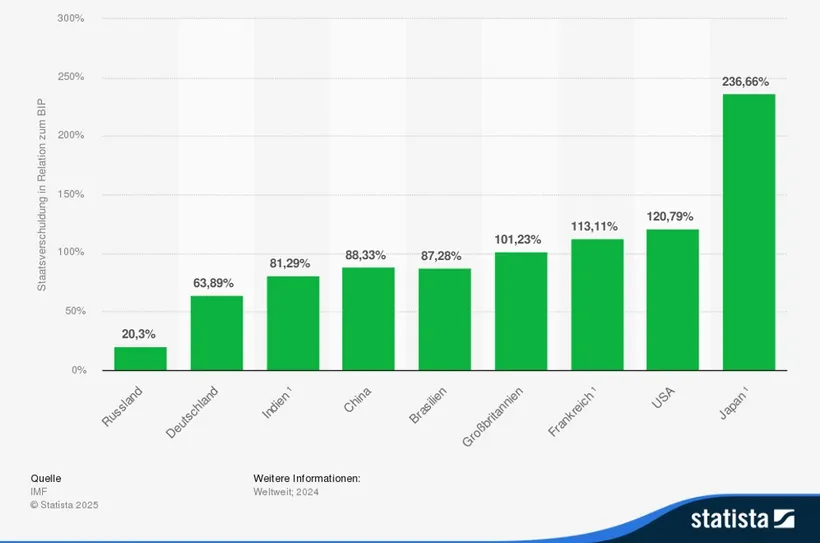

Government debt in the most important industrialised and emerging countries in 2024 relative to the GDP

Sources: IMF, Statista, data as of April 2025

Fiscal dominance

This raises the spectre of a scenario known as fiscal dominance. In this environment, the monetary policy is constrained (“dominated”) by the requirements of fiscal policy. This means that the central bank cannot pursue its monetary policy objectives independently because it has to take the financing of the national budget into account. This can jeopardise price stability, which is usually defined as inflation of 2% in the medium term.

Technological developments

This does not necessarily suggest excessive inflation for the future. Technological developments such as those in the field of artificial intelligence could lead to an increase in productivity and dampen prices. Or it could turn out that the AI boom has led to a sense of overshooting on the equity markets. The bursting of the bubble would generate falling inflationary pressure (disinflation). In addition, countries could agree to switch to a tough austerity policy, as they did after the Great Financial Crisis of 2008/2009. That period was indeed characterised by excessively low inflation (below 2%). The degree of political pressure is also a decisive factor.

Unconventional US policy

In general, most central banks enjoy a high level of credibility when it comes to achieving their inflation targets. However, the US administration's policy is unconventional in many respects. For example, in the summer of 2025, US President Donald Trump publicly called for the Federal Reserve to lower its key-lending rate to 1%. This would make it easier to finance the high level of government debt and give the economy and the equity market a boost. In fact, the US administration is exerting considerable political pressure on the Fed to lower key-lending rates both significantly and fast. For example, Stephen Miran, Chairman of the Council of Economic Advisors (the President's Council of Economic Advisors), has filled a vacant position on the Fed's Interest Rate Committee (and suspended his office).

The independence of the Fed is being eroded from multiple sides:

- Institutional independence: the US President has repeatedly issued “instructions” to lower key-lending rates. Secretary of the Treasury Scott Bessent also spoke out in favour of a lower key-lending rate (of 3%). In fact, the Fed cut rates in September, even though the economic forecasts in the Fed's Summary of Economic Projections did not support this move. “Only” the labour market shows downside risks.

- Personnel independence: the US administration's efforts to dismiss Lisa Cook have not yet been successful.

- Financial independence: the Fed has its own budget. However, the construction of the new Fed building was heavily criticised by politicians due to allegedly excessive costs.

Summary

Nothing bad has happened yet. Central banks still enjoy a high level of credibility on the bond market. Not only in terms of economic growth and the financial markets, but also in the area of monetary policy, “resilience to negative influences” appears to be an important feature. That being said, the risk of central banks losing their independence is particularly evident in the sharp rise in the price of gold (see our article “Focus on gold”). While this may be excessive, the main argument remains the same: the independence of central banks is under pressure. It is probably no coincidence that the US dollar has lost more ground against gold than the euro. This is because pressure on the central bank is already explicit in the USA. In other countries, it is a result of high government debt.

For explanations of technical terms, please visit our Fund Glossary.

Disclaimer

This document is an advertisement. Please refer to the prospectus of the UCITS or to the Information for Investors pursuant to Art 21 AIFMG of the alternative investment fund and the Key Information Document before making any final investment decisions. All data is sourced from Erste Asset Management GmbH, unless indicated otherwise. Our languages of communication are German and English.

The prospectus for UCITS (including any amendments) is published in accordance with the provisions of the InvFG 2011 in the currently amended version. Information for Investors pursuant to Art 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in connection with the InvFG 2011.

The fund prospectus, Information for Investors pursuant to Art 21 AIFMG, and the Key Information Document can be viewed in their latest versions at the website www.erste-am.com within the section mandatory publications or obtained in their latest versions free of charge from the domicile of the management company and the domicile of the custodian bank. The exact date of the most recent publication of the fund prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the Key Information Document are available, and any additional locations where the documents can be obtained can be viewed on the website www.erste-am.com. A summary of investor rights is available in German and English on the website www.erste-am.com/investor-rights as well as at the domicile of the management company.

The management company can decide to revoke the arrangements it has made for the distribution of unit certificates abroad, taking into account the regulatory requirements.

Detailed information on the risks potentially associated with the investment can be found in the fund prospectus or Information for investors pursuant to Art 21 AIFMG of the respective fund. If the fund currency is a currency other than the investor's home currency, changes in the corresponding exchange rate may have a positive or negative impact on the value of his investment and the amount of the costs incurred in the fund - converted into his home currency.

Our analyses and conclusions are general in nature and do not take into account the individual needs of our investors in terms of earnings, taxation, and risk appetite. Past performance is not a reliable indicator of the future performance of a fund.

The issue and redemption of unit certificates and the execution of payments to unit holders has been transferred to the Fund's custodian bank/depositary, Erste Group Bank AG, Am Belvedere 1, 1100 Vienna, Austria. Redemption requests can be submitted by investors to their custodian bank, which will forward them to the Custodian Bank/Depositary of the Fund for execution via the usual banking channels. All payments to investors are also processed via the usual banking clearing channel with the investor's custodian bank. In Germany, the issue and return prices of shares are published in electronic form on the web site www.erste-am.com (and also at www.fundinfo.com). Any other information for Shareholders is published in the Bundesanzeiger, Cologne.