Focus on gold

Overheated rally or sustainable allocation opportunity?

In a world stumbling from one crisis to the next, many institutional investors see no alternative to the world's oldest currency: gold. As a result, the gold price is currently moving in only one direction – upwards. It has doubled in less than two years and broke through the historic mark of USD 4,000 per ounce for the first time at the beginning of October (data from Refinitiv Datastream). In a discussion about the capital market and its background, Daniel Feix, Managing Director of Impact Asset Management, and Andreas Böger, Fund Manager of ERSTE STOCK GOLD, assessed the further prospects for Erste Asset Management's access to investments in the precious metal.

Gold is traditionally considered a safe haven for institutional investors: it is not tied to any particular currency or nation and has steadily increased in value over time. Although, unlike securities, this coveted precious metal does not offer any returns, its low risk has secured it a place in many investment portfolios. Please note: investing in gold and securities involves both opportunities and risks.

Rising gold price despite increased interest rates

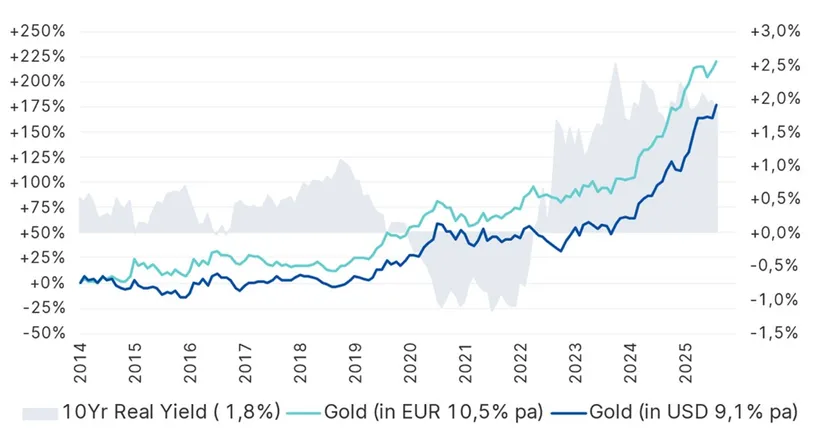

In an environment of falling interest rates and geopolitical uncertainty, gold has always been particularly sought after as an alternative investment. However, Daniel Feix emphasises that the current development has some peculiarities. In the past, the gold price would regularly rise when real interest rates were low. However, it would then fall again when interest rates were high. “Since 2022, this formula no longer applies,” as Feix analyses the situation. “Despite rising interest rates, the gold price continued to rise.” Most recently, it has – metaphorically speaking – exploded, gaining more than 50% in the year to date alone.

Correlation between interest rates and gold price

Past performance is not indicative of future value development.

- Low real interest rates -> rising gold prices (historically)

- High real interest rates -> falling gold prices (historically)

Sources: Impact Asset Management, Erste Asset Management, data as of 30 August 2025

The reasons for the gold rush

Economists around the world are concerned about the debt levels of industrialised nations. While France and the United Kingdom stand out negatively in Europe, many are particularly concerned about the financial development of the United States. The USA currently has debt outstanding of USD 37.8 trillion, which corresponds to a debt ratio of 125%. As a consequence of this development, central banks have significantly increased their gold reserves in recent years in order to reduce their counterparty risk and diversify their reserves – a sign of the growing role of the precious metal as a store of value and protection against inflation. However, investing in gold also comes with risks.

Another reason for the sharp increase in the gold price lies in the US sanctions against Russian foreign exchange reserves following the attack on Ukraine. These sanctions had little effect, as Russia was able to draw on its extensive gold reserves. Other countries, including China, drew their own conclusions and also increased their gold purchases – with noticeable consequences for the gold price.

Most recently, a psychological factor has also come into play as a price driver: many investors have jumped on the bandwagon so as not to miss out and to participate in the current gold rush.

For the time being, there is no end in sight to this development. Many experts and analysts believe that the gold rally could continue. Daniel Feix also shares this view. In times of rising government debt, declining confidence in national currencies, and a world full of multi-pronged crises, the precious metal remains an attractive safe haven, he believes.

Why gold companies are shining as we speak

An interesting aspect for institutional investors: in the shadow of the rapid gold price rally, companies operating along the supply chain of the world's oldest currency are also benefiting from the current gold rush.

Andreas Böger, fund manager of ERSTE STOCK GOLD, points out a special “gold nugget effect” for the shareholders of these companies in this context: “While the price of gold has risen from about USD 1,100 to over USD 4,000 per ounce over the past ten years, production costs have only increased moderately from about USD 1,000 to USD 1,600. As a result, the industry's operating margin has soared to a record level.”

In addition to investing in physical gold, such as gold bars, gold coins, or jewellery, investors may also want to consider gold shares as an alternative. “Gold shares offer access to various segments of the value chain and can serve as leverage when prices rise,” Böger emphasises. Please note: investing in securities involves both opportunities and risks.

The leverage effect of gold mining equities is that rising gold prices can have a disproportionate impact on profit margins, depending on the development of production costs. “Recently, these factors have led to a significant increase in profit margins,” Böger explains. However, this leverage effect can also have a negative effect if the gold price falls or production costs rise.

Andreas Böger, Fund manager of ERSTE STOCK GOLD, picture credit: Tim Dornaus epilogy.photography

The entire gold sector as investment universe

ERSTE STOCK GOLD offers the opportunity to invest in the entire supply chain of this shining classic with a flexible capital allocation. Global gold production in 2024 totalled approximately 3,300 tonnes, dominated by countries such as China, Russia, Australia, and Canada. The equity fund focuses on the various areas of companies involved in gold production:

- Producers: companies that mine gold and participate directly in the gold price.

- Developers: companies that develop mines and are about to start production.

- Explorers: companies that search for new gold deposits.

- Royalty/streamers: mining financiers who participate in the revenues and profits of mines without mining themselves.

Focus on medium-sized producers

Many analysts are focusing on medium-sized producers in particular, as they are often more agile and experience stronger growth than large index heavyweights. The valuation for these “gold nuggets” is historically attractive: the average price-earnings ratio (P/E) for the sector has fallen from 25–35x (2014) to 10–15x (2025) (source: Bloomberg).

The ERSTE STOCK GOLD fund pursues an active allocation strategy across various segments of the gold sector and adapts to the market phase prevalent at the time. The focus is on medium-sized gold producers. The portfolio is complemented by the addition of developers, explorers, and royalty/streaming mining companies. The weighting is currently about 80% gold and 20% silver.

When asked about the fund's investment focus, fund manager Andreas Böger highlights companies with strong management, good growth prospects, and solid fundamentals. “At the same time, we avoid investments in large index heavyweights, companies with very high gold production and problematic growth prospects,” he explains.

A look at the fund's performance over the past ten years shows that this strategy has yielded positive results in the long term. However, past performance is no reliable indicator of the fund's future performance.

Significant risks

Investments in the gold sector may be subject to significant fluctuations in value. In addition to sector-specific risk, there are issuer risks, exchange rate risks for foreign currency exposure, and operational risks. A loss of capital cannot be ruled out. Institutional investors should carefully examine credit, liquidity, deposit, and derivative risks in particular, as well as the regulatory framework in accordance with the Alternative Investment Fund Managers Act (AIFMG). For detailed risk information, please refer to the fund prospectus.

Opportunities and risks at a glance

Advantages for institutional clients

Broadly diversified investment in gold companies with little capital investment.

Active stock selection based on fundamental criteria.

Opportunities for capital appreciation.

The fund is suitable as an addition to an existing equity portfolio and is intended for long-term capital appreciation.

Risks to be considered

The price of the funds can fluctuate greatly (high volatility).

The investor mainly bears the risk of the commodity sector as well as the issuer risk of the participating companies.

Due to the investment in foreign currencies, the net asset value in Euro can fluctuate due to changes in the exchange rate.

Loss of capital is possible.

Risks that may be significant for the fund are in particular: credit and counterparty risk, liquidity risk, custody risk, derivative risk and operational risk. Comprehensive information on the risks of the fund can be found in the prospectus or the information for investors pursuant to § 21 AIFMG, section II, ""Risk information"".

For explanations of technical terms, please visit our Fund Glossary.

Disclaimer

This document is an advertisement. Please refer to the prospectus of the UCITS or to the Information for Investors pursuant to Art 21 AIFMG of the alternative investment fund and the Key Information Document before making any final investment decisions. All data is sourced from Erste Asset Management GmbH, unless indicated otherwise. Our languages of communication are German and English.

The prospectus for UCITS (including any amendments) is published in accordance with the provisions of the InvFG 2011 in the currently amended version. Information for Investors pursuant to Art 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in connection with the InvFG 2011.

The fund prospectus, Information for Investors pursuant to Art 21 AIFMG, and the Key Information Document can be viewed in their latest versions at the website www.erste-am.com within the section mandatory publications or obtained in their latest versions free of charge from the domicile of the management company and the domicile of the custodian bank. The exact date of the most recent publication of the fund prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the Key Information Document are available, and any additional locations where the documents can be obtained can be viewed on the website www.erste-am.com. A summary of investor rights is available in German and English on the website www.erste-am.com/investor-rights as well as at the domicile of the management company.

The management company can decide to revoke the arrangements it has made for the distribution of unit certificates abroad, taking into account the regulatory requirements.

Detailed information on the risks potentially associated with the investment can be found in the fund prospectus or Information for investors pursuant to Art 21 AIFMG of the respective fund. If the fund currency is a currency other than the investor's home currency, changes in the corresponding exchange rate may have a positive or negative impact on the value of his investment and the amount of the costs incurred in the fund - converted into his home currency.

Our analyses and conclusions are general in nature and do not take into account the individual needs of our investors in terms of earnings, taxation, and risk appetite. Past performance is not a reliable indicator of the future performance of a fund.

The issue and redemption of unit certificates and the execution of payments to unit holders has been transferred to the Fund's custodian bank/depositary, Erste Group Bank AG, Am Belvedere 1, 1100 Vienna, Austria. Redemption requests can be submitted by investors to their custodian bank, which will forward them to the Custodian Bank/Depositary of the Fund for execution via the usual banking channels. All payments to investors are also processed via the usual banking clearing channel with the investor's custodian bank. In Germany, the issue and return prices of shares are published in electronic form on the web site www.erste-am.com (and also at www.fundinfo.com). Any other information for Shareholders is published in the Bundesanzeiger, Cologne.