Global economic and financial market outlook

Global weakening in the coming months

We expect global economic growth to slow noticeably in the coming months. Growth rates of just 2.3% are expected for 2025, falling further to 2.1% in 2026. This development is well below long-term potential and reflects a number of structural factors. These include, in particular, protectionist tendencies in global trade, an erratic US trade policy, and the cyclical slowdown in global industrial production.

A key negative factor is the average US tariff rate of about 15%, which not only represents a moderate stagflationary impulse for the US economy, but also noticeably dampens global demand. Although the temporary suspension of reciprocal tariffs has brightened corporate sentiment somewhat and reduced the risks of recession, uncertainty remains high. Global industrial production is already showing the first signs of weakness following the expiry of pull-forward effects.

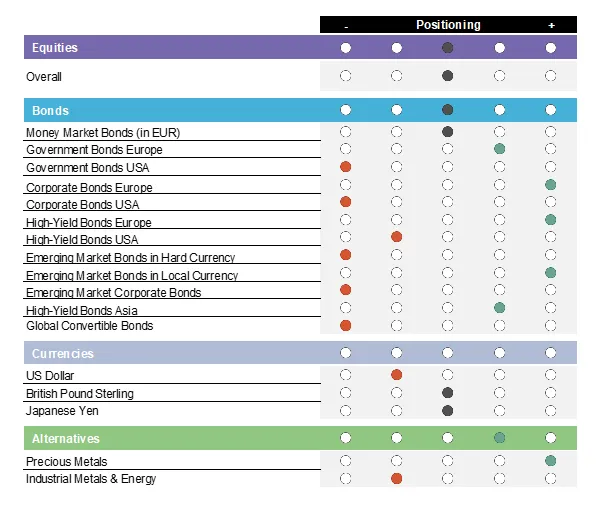

Equity markets: defensive stance with targeted adjustment

In the equity sector, we raised the previous underweight position to neutral. This decision was based on the assessment that the immediate risks of recession had decreased. That being said, the environment remains challenging, as demonstrated by the recent military conflict between Israel and Iran. The US attack on three Iranian nuclear facilities on the night of 22 June could trigger countermeasures and escalate the conflict. The risk of a further rise in oil prices has increased and would hit the equity markets. Please note the opportunities and risks associated with investing.

Regional and sector allocations reflect our defensive stance. The United States is underweight due to high valuations, political uncertainty, and growth risks. By contrast, we favour defensive sectors such as US healthcare companies and high-dividend European equities. We see opportunities in the recovery of US growth equities, in European small caps, which are benefiting from interest rate cuts, and in value shares with attractive valuations and fiscal stimulus.

Bonds: selective overweight amid global risk assessment

In the bond segment, we have maintained a neutral duration, as inflation risks in the USA are offset by global growth risks. Regionally, we are overweighting the Eurozone, as weak growth and declining inflation there are creating a favourable environment for bonds. US bonds, on the other hand, remain underweighted, as they are weighed down by stagflationary tendencies and a loss of confidence.

Local currency bonds from emerging markets appear particularly attractive to us as they are benefiting from monetary easing. However, we avoid hard currency bonds from these regions as they are heavily dependent on the US interest rate environment. We have also reduced the previous overweight in the money market to neutral, a move that reflects the easing of tensions following the suspension of US retaliatory tariffs.

Commodities and precious metals: gold as strategic anchor

In the commodities sector, the focus is clearly on gold, which we overweight. There are many reasons for this: the ongoing trade conflict, inflation and sovereign debt risks, expected key-lending rate cuts, and discussions about a possible reorganisation of the global financial system are strengthening gold's role as a safe haven. In addition, the erosion of confidence in the US dollar is contributing to the appeal of the precious metal.

Industrial metals, on the other hand, remain underweighted. The global slowdown in growth, particularly as a result of tariffs, and weak demand from China mean that we do not expect any form of recovery here in the short term.

Currencies: US dollar under pressure

Our defensive stance is also evident in the currency arena. The unorthodox and erratic US policy has significantly weakened the attractiveness of the US dollar. By comparison, the euro appears more stable, supported by fiscal measures and a relatively predictable political situation.

Source: Erste Asset Management, June 2025

For explanations of technical terms, please visit our Fund Glossary.

Notes: Forecasts are not a reliable indicator of future performance. Where fund portfolio positions are disclosed in this document, they are based on market developments as at 5 June 2025. These portfolio positions may change at any time as part of active management. Please note that investing in securities involves risks as well as the opportunities described.

Disclaimer

This document is an advertisement. Please refer to the prospectus of the UCITS or to the Information for Investors pursuant to Art 21 AIFMG of the alternative investment fund and the Key Information Document before making any final investment decisions. All data is sourced from Erste Asset Management GmbH, unless indicated otherwise. Our languages of communication are German and English.

The prospectus for UCITS (including any amendments) is published in accordance with the provisions of the InvFG 2011 in the currently amended version. Information for Investors pursuant to Art 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in connection with the InvFG 2011.

The fund prospectus, Information for Investors pursuant to Art 21 AIFMG, and the Key Information Document can be viewed in their latest versions at the website www.erste-am.com within the section mandatory publications or obtained in their latest versions free of charge from the domicile of the management company and the domicile of the custodian bank. The exact date of the most recent publication of the fund prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the Key Information Document are available, and any additional locations where the documents can be obtained can be viewed on the website www.erste-am.com. A summary of investor rights is available in German and English on the website www.erste-am.com/investor-rights as well as at the domicile of the management company.

The management company can decide to revoke the arrangements it has made for the distribution of unit certificates abroad, taking into account the regulatory requirements.

Detailed information on the risks potentially associated with the investment can be found in the fund prospectus or Information for investors pursuant to Art 21 AIFMG of the respective fund. If the fund currency is a currency other than the investor's home currency, changes in the corresponding exchange rate may have a positive or negative impact on the value of his investment and the amount of the costs incurred in the fund - converted into his home currency.

Our analyses and conclusions are general in nature and do not take into account the individual needs of our investors in terms of earnings, taxation, and risk appetite. Past performance is not a reliable indicator of the future performance of a fund.

The issue and redemption of unit certificates and the execution of payments to unit holders has been transferred to the Fund's custodian bank/depositary, Erste Group Bank AG, Am Belvedere 1, 1100 Vienna, Austria. Redemption requests can be submitted by investors to their custodian bank, which will forward them to the Custodian Bank/Depositary of the Fund for execution via the usual banking channels. All payments to investors are also processed via the usual banking clearing channel with the investor's custodian bank. In Germany, the issue and return prices of shares are published in electronic form on the web site www.erste-am.com (and also at www.fundinfo.com). Any other information for Shareholders is published in the Bundesanzeiger, Cologne.