The new “charm” of European bonds

Status quo on the bond market

The conditions for investors in the bond market have changed significantly in recent months. Following the interest rate turnaround, the money market initially offered higher yields. The European Central Bank (ECB) has now brought interest rates back to around the current and long-term target inflation rate of around 2%. This has caused the yield curve to steepen, a sign that the interest rate policy is returning to normal. Investing in the bond market involves both opportunities and risks.

Challenges in recent years

In recent years, bonds have struggled to keep pace with money market returns. Reasons for this include:

- Rising inflation expectations

- Concerns about the long-term government debt of specific countries

- No economic slowdown despite an inverted yield curve

These factors have led to many investors taking a cautious approach to bonds.

New momentum from fiscal policy

Additional momentum came from Germany: the announcement of a comprehensive spending package for defence and infrastructure was reminiscent of the yield movements at the time of German reunification – albeit at a significantly different interest rate level than back then.

At least one further interest rate cut is currently expected in the Eurozone, while a pause in interest rate hikes is the likely scenario for the USA. If inflationary pressures were to arise there as a result of new tariffs, interest rate cuts could soon follow in the United States as well.

Why European bonds are attractive again

There are currently a number of arguments in favour of investing in European bonds:

- Declining attractiveness of the money market, particularly in terms of real yields

- Stable inflation expectations in the Eurozone, in contrast to the USA, where tariffs could cause price spikes in the short term

- Possible return of deflationary trends due to Chinese exports

It remains to be seen whether and to what extent cheap Chinese goods will reach the European market. From a global perspective, however, China is likely to provide further deflationary impetus. But there are also risks on the capital market.

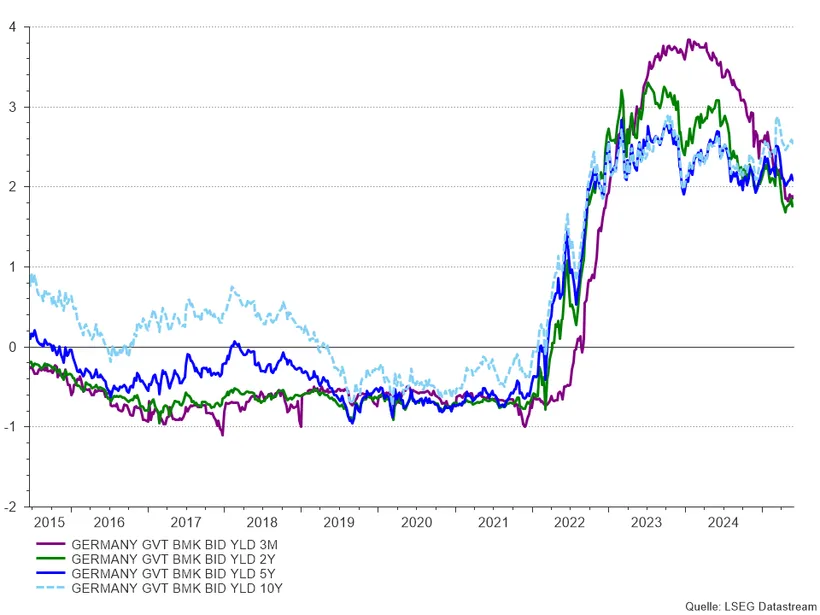

Interest rate development of German government bonds (2015–2025): yields across various maturities

Past performance is no reliable indicator of future development.

Source: LSEG Datastream, as of 31 May 2025

The chart shows the yields of German government bonds with different maturities:

- GE 3M (purple): yield on three-month money market instruments

- GE 2Y (green): yield on two-year German government bonds

- GE 5Y (dark blue): yield on five-year German government bonds

- GE 10Y (light blue): yield on ten-year German government bonds

The euro as alternative to the US dollar?

The status of US Treasury bonds and the US dollar as dominant investment instruments is increasingly being called into question. In a multipolar world order, a clear replacement is unlikely to emerge, but the European bond market is gaining importance as a serious alternative.

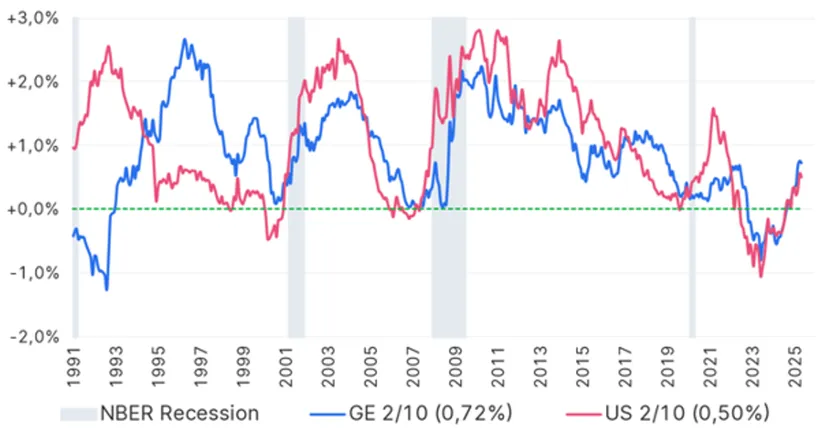

Yield curves USA vs. Germany (1991–2025): development of the difference between 10Y and 2Y government bonds

Past performance is no reliable indicator of future development.

Source: Erste Asset Management, monthly data, as of 31 May 2025

The chart shows the yield curve, in this case the difference between long-term (10Y) and short-term (2Y) government bonds, for Germany (representing the Eurozone) and the United States over more than three decades.

What the chart shows:

- Normal yield curve: when the line is above 0%, long-term interest rates are higher than short-term rates – a sign of economic growth and stable expectations.

- Yield curve inversion: when the line falls below 0%, short-term interest rates are higher than long-term rates – often an early indicator of a recession, as was the case in 2001 and 2007.

- Since 2022: both curves are inverted in both the USA and Germany. This points to a restrictive monetary policy and a possible economic slowdown.

- Historical context: previous inversions (e.g. 2000, 2006) were often preceded by recessions – as shown by the grey NBER recession phases.

Risks from rising government debt

On the flip side, many countries are facing growing debt levels. Germany has long been regarded as a symbol of fiscal stability – not the least due to its debt brake. Under the new government led by Chancellor Friedrich Merz, it remains to be seen whether and how Germany will return to budgetary discipline. The impact on other Eurozone countries is also not clear at this point.

In the short term, some countries have already seen their credit ratings downgraded. In the long term, however, an economic upturn could improve the budgetary situation. If the Eurozone managed to boost its structurally weak potential growth (which results from demographic factors), slightly higher yields would also be justified.

Assessment by Erste Asset Management

From Erste Asset Management's perspective, several factors currently favour exposure to the European bond market. Within the available spectrum, we consider investment-grade corporate bonds particularly attractive. Despite their current low spreads relative to government bonds, they offer a yield advantage combined with moderate duration – a balanced risk/return profile.

Another point on the pro side is the fact that real positive returns appear possible in the foreseeable future. Despite international trade conflicts, the credit quality of issuers does not appear to have been negatively affected across the board.

Conclusion: attractive perspectives for euro bonds

The positive arguments in favour of bonds from the Eurozone currently outweigh the negative ones. Particularly noteworthy is the steep yield curve, which offers a certain buffer against losses. Higher initial yields can cushion potential declines in prices – an advantage in a volatile market environment.

For explanations of technical terms, please visit our Fund Glossary.

Disclaimer

This document is an advertisement. Please refer to the prospectus of the UCITS or to the Information for Investors pursuant to Art 21 AIFMG of the alternative investment fund and the Key Information Document before making any final investment decisions. All data is sourced from Erste Asset Management GmbH, unless indicated otherwise. Our languages of communication are German and English.

The prospectus for UCITS (including any amendments) is published in accordance with the provisions of the InvFG 2011 in the currently amended version. Information for Investors pursuant to Art 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in connection with the InvFG 2011.

The fund prospectus, Information for Investors pursuant to Art 21 AIFMG, and the Key Information Document can be viewed in their latest versions at the website www.erste-am.com within the section mandatory publications or obtained in their latest versions free of charge from the domicile of the management company and the domicile of the custodian bank. The exact date of the most recent publication of the fund prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the Key Information Document are available, and any additional locations where the documents can be obtained can be viewed on the website www.erste-am.com. A summary of investor rights is available in German and English on the website www.erste-am.com/investor-rights as well as at the domicile of the management company.

The management company can decide to revoke the arrangements it has made for the distribution of unit certificates abroad, taking into account the regulatory requirements.

Detailed information on the risks potentially associated with the investment can be found in the fund prospectus or Information for investors pursuant to Art 21 AIFMG of the respective fund. If the fund currency is a currency other than the investor's home currency, changes in the corresponding exchange rate may have a positive or negative impact on the value of his investment and the amount of the costs incurred in the fund - converted into his home currency.

Our analyses and conclusions are general in nature and do not take into account the individual needs of our investors in terms of earnings, taxation, and risk appetite. Past performance is not a reliable indicator of the future performance of a fund.

The issue and redemption of unit certificates and the execution of payments to unit holders has been transferred to the Fund's custodian bank/depositary, Erste Group Bank AG, Am Belvedere 1, 1100 Vienna, Austria. Redemption requests can be submitted by investors to their custodian bank, which will forward them to the Custodian Bank/Depositary of the Fund for execution via the usual banking channels. All payments to investors are also processed via the usual banking clearing channel with the investor's custodian bank. In Germany, the issue and return prices of shares are published in electronic form on the web site www.erste-am.com (and also at www.fundinfo.com). Any other information for Shareholders is published in the Bundesanzeiger, Cologne.